Braid — Core Banking Dashboard

Braid is banking infrastructure that lets community banks sponsor fintech programs. I built its core dashboard — the surface where banks run ledger, payments, fraud, and compliance operations.

See the impact ↓In the box

The problem

Braid deploys a 'sidecar core' beside a bank's existing core system, giving community banks the rails to sponsor fintech programs — virtual accounts, a real-time ledger, and direct access to FedNow, ACH, wire, and RTP. All of that power needed one operational surface: a dashboard where bank teams post and reconcile transactions, manage programs, and stay compliant. Legacy tools weren't built for any of this.

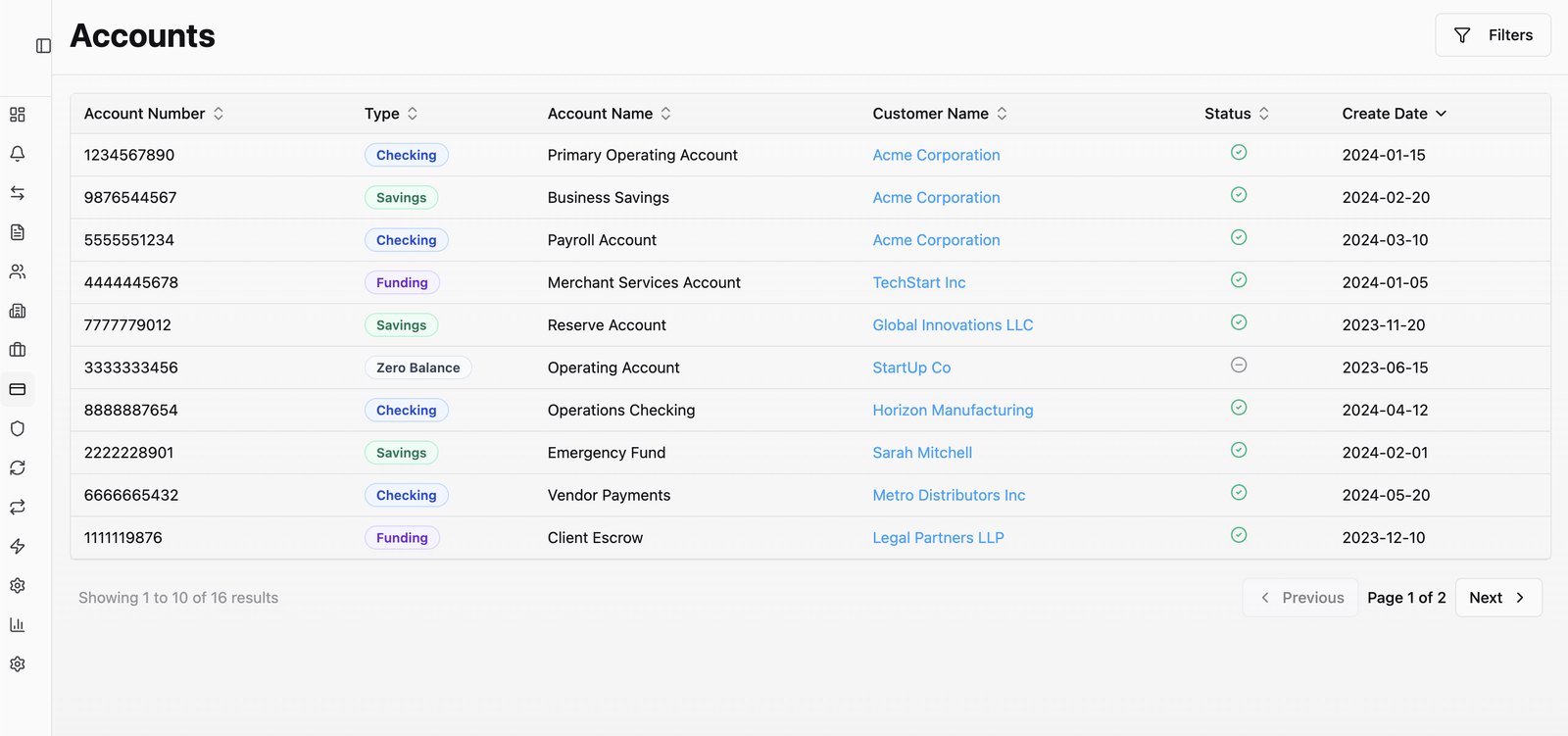

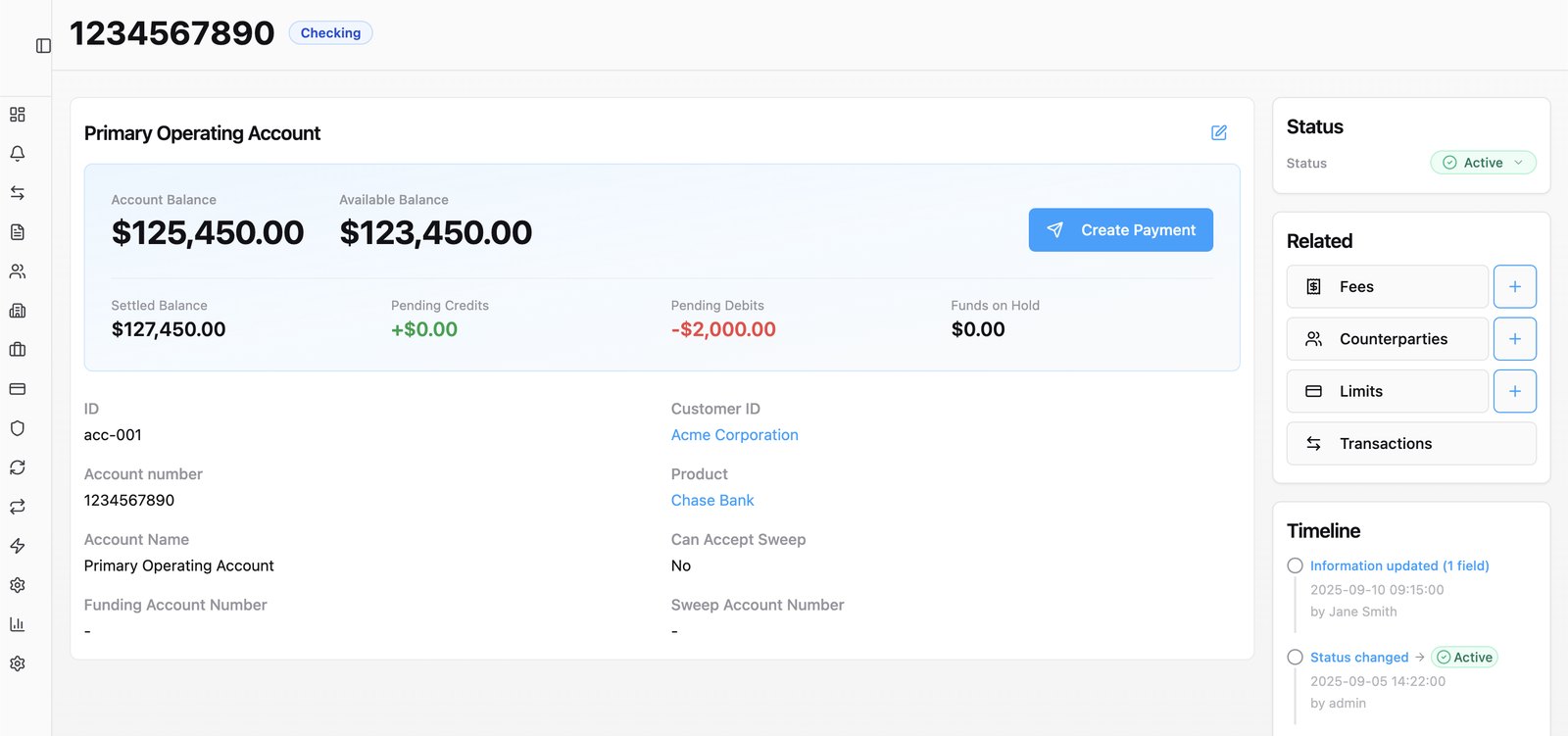

The Accounts module — types, ownership, and status across the whole book (demo data).

Accounts, in one operational view

Every account a bank runs — checking, savings, funding, escrow — in a single sortable table, and one click deeper the full picture of any account: live, available, and settled balances, pending credits and debits, funds on hold, related fees, limits and counterparties, plus payment creation and a full audit timeline.

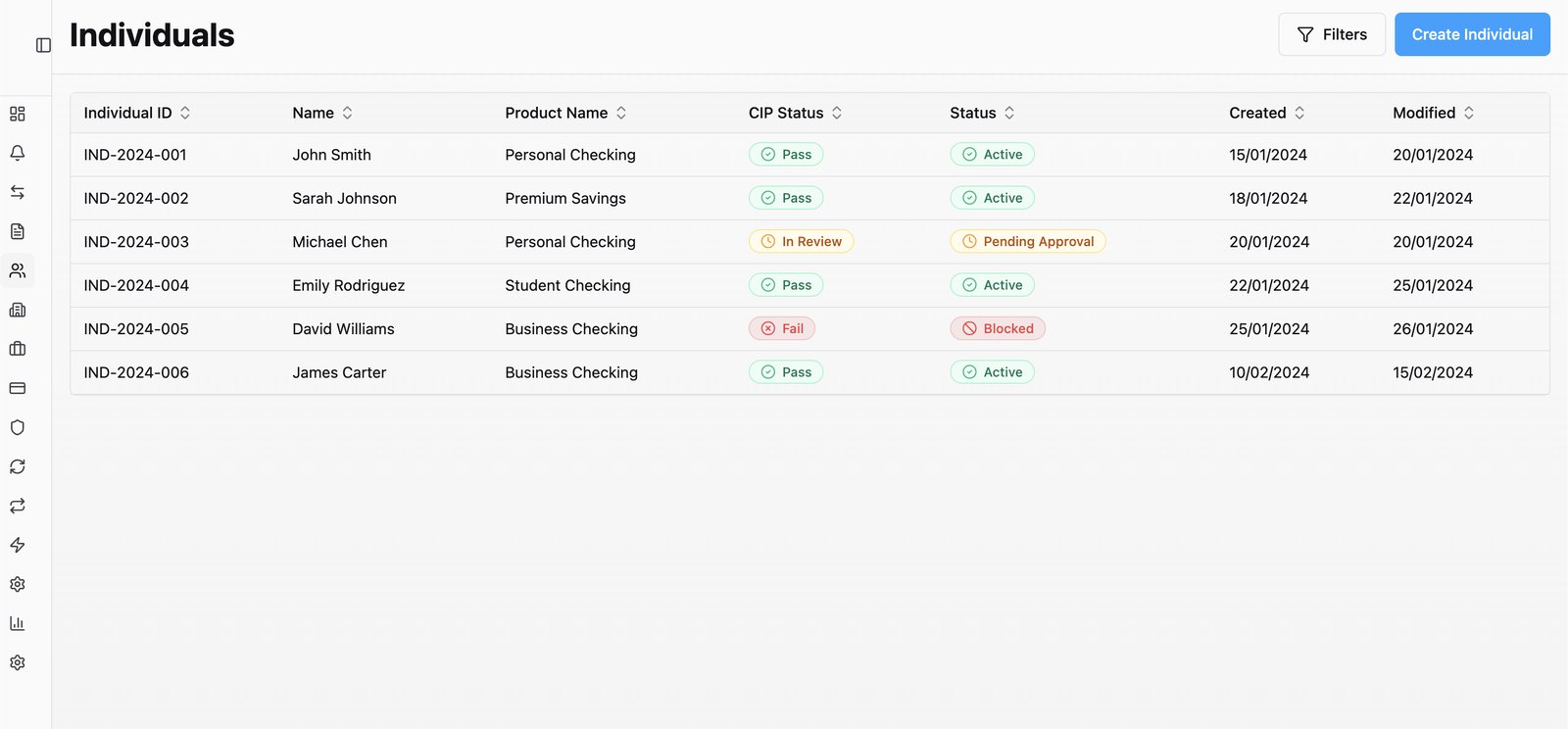

Individuals list with CIP status.

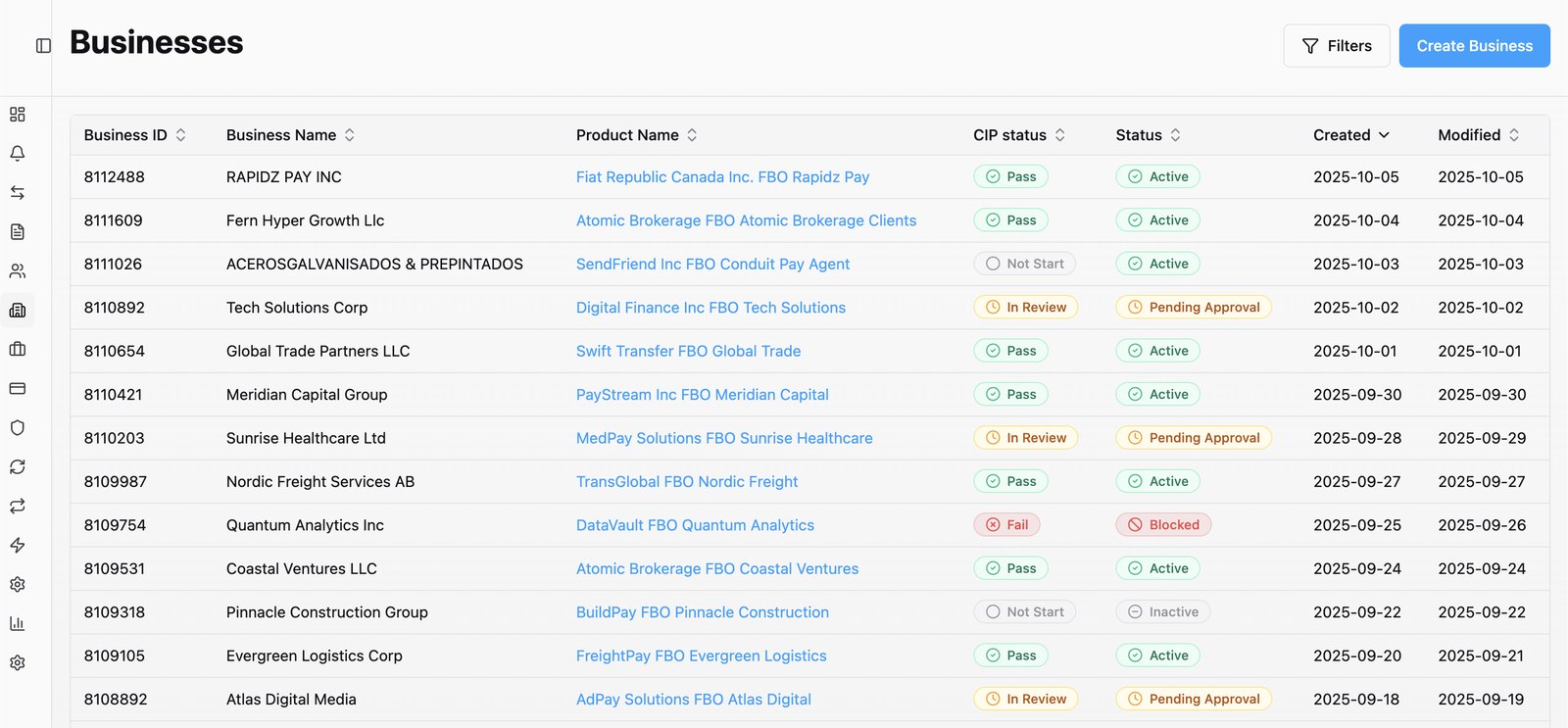

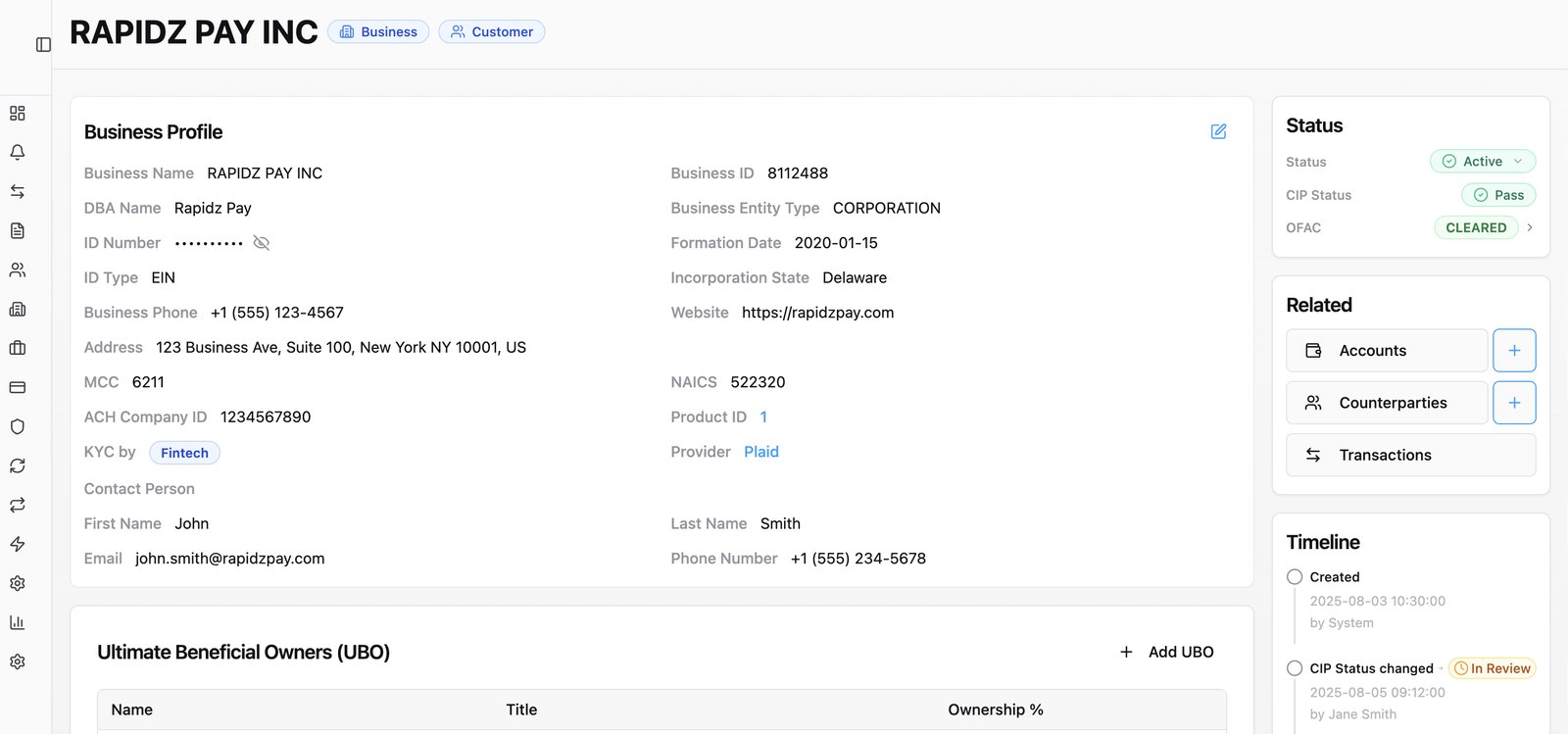

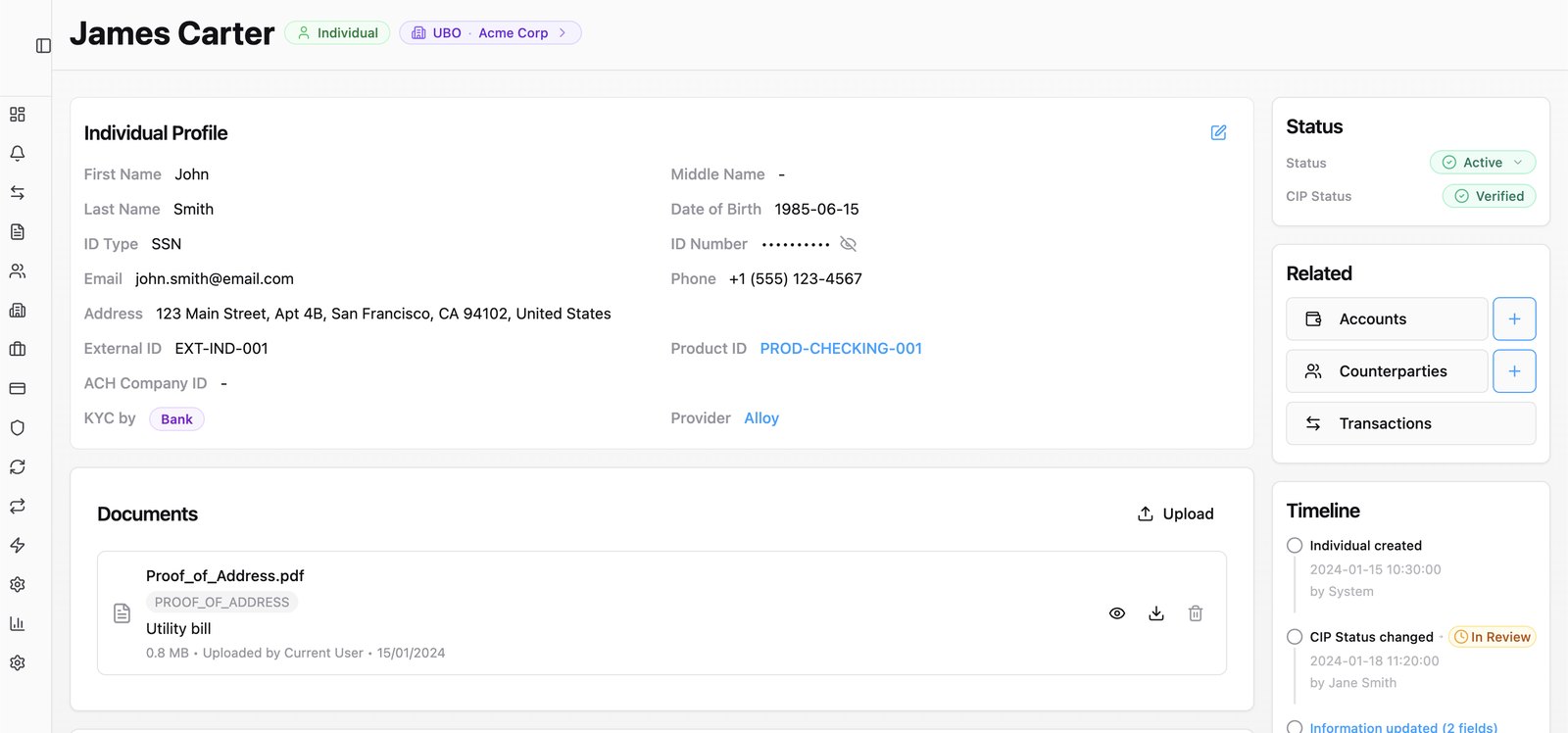

Customers and KYC

Individuals and businesses from list to profile: CIP verification status sits in every row, and one click deeper is the full KYC picture — business profiles with beneficial owners, OFAC clearance, masked IDs, and audit timelines; individual profiles with identity documents, KYC provider, and product assignment. Fintech-sponsored customers carry their FBO product lineage right in the table.

Transaction detail — status, OFAC screening, and compliance timeline.

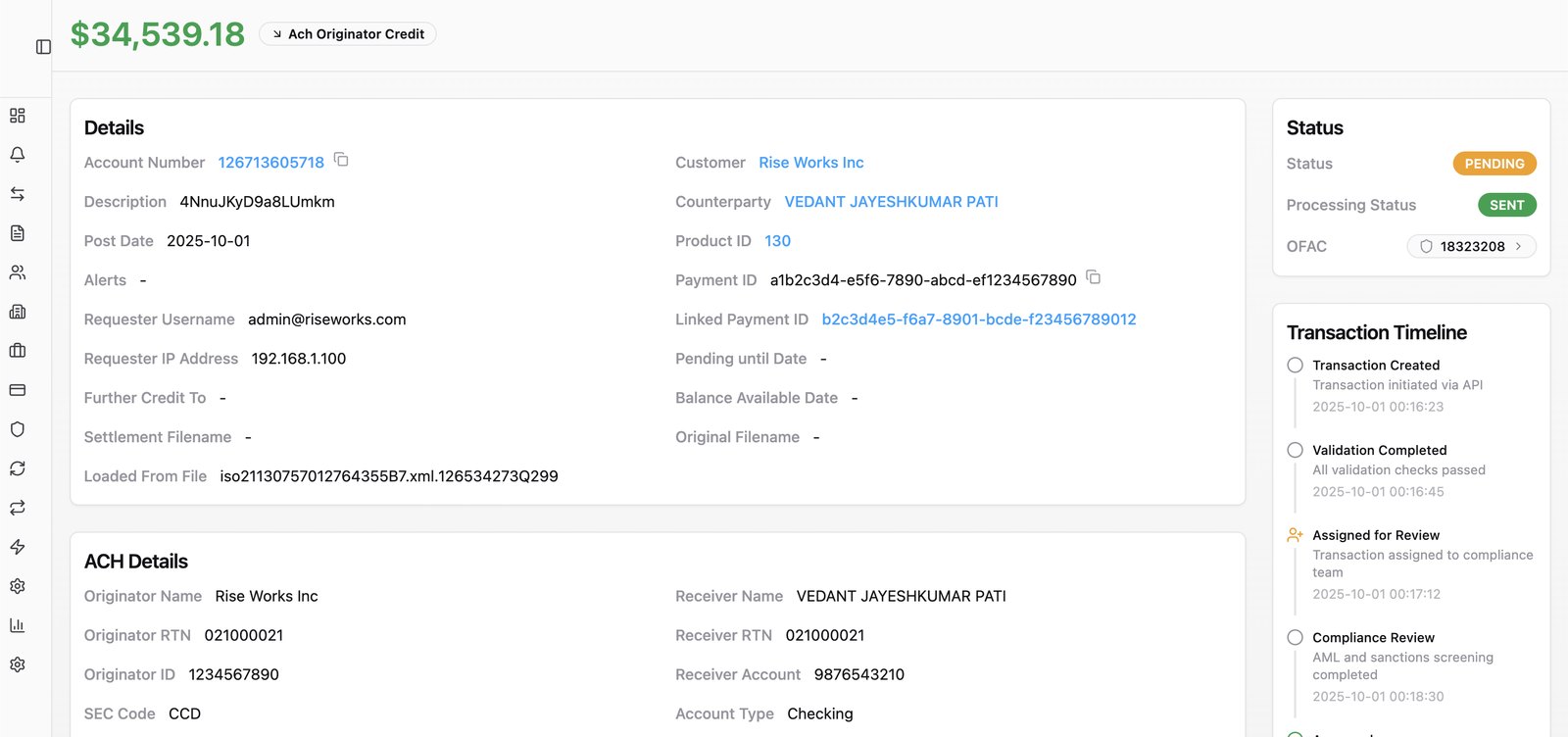

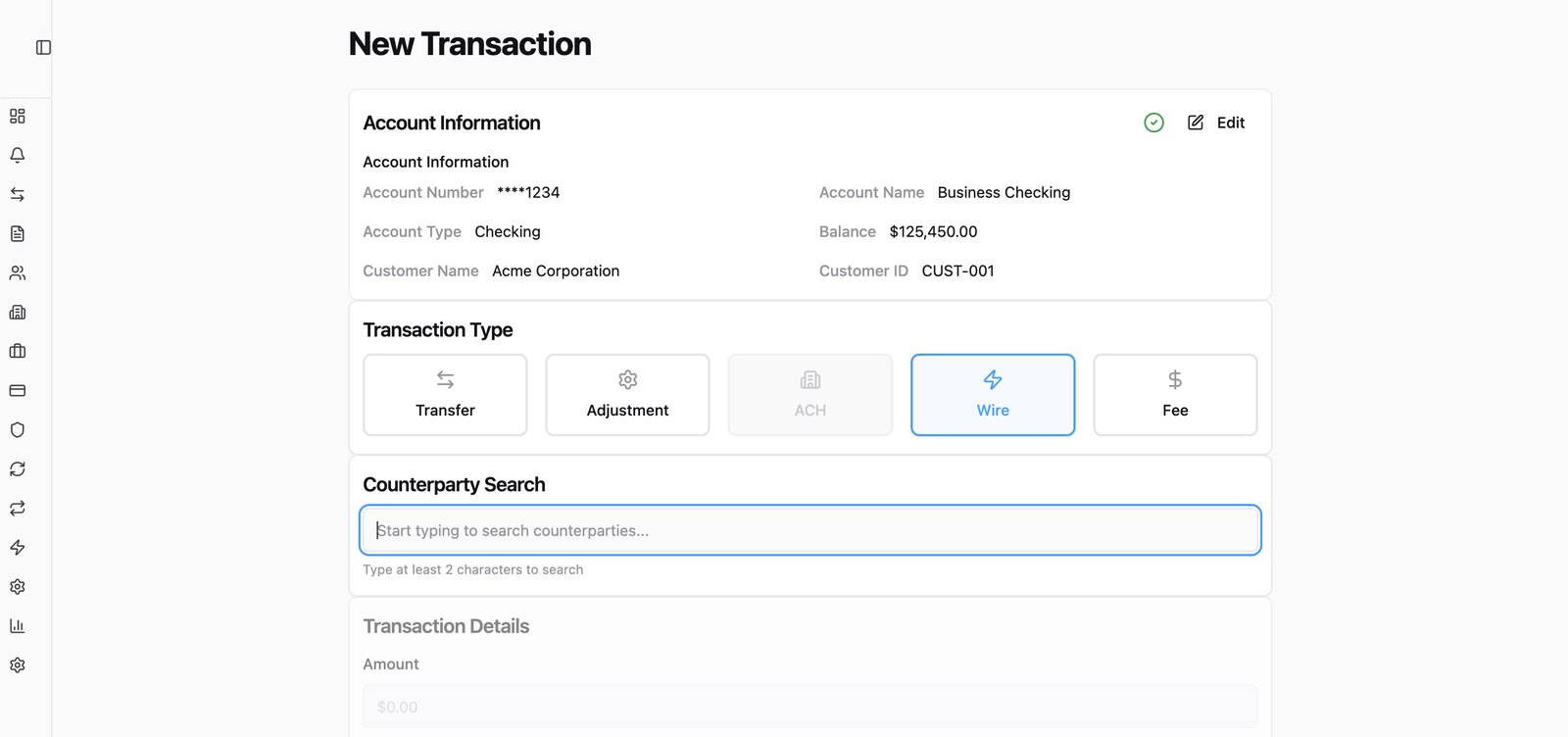

Payment operations

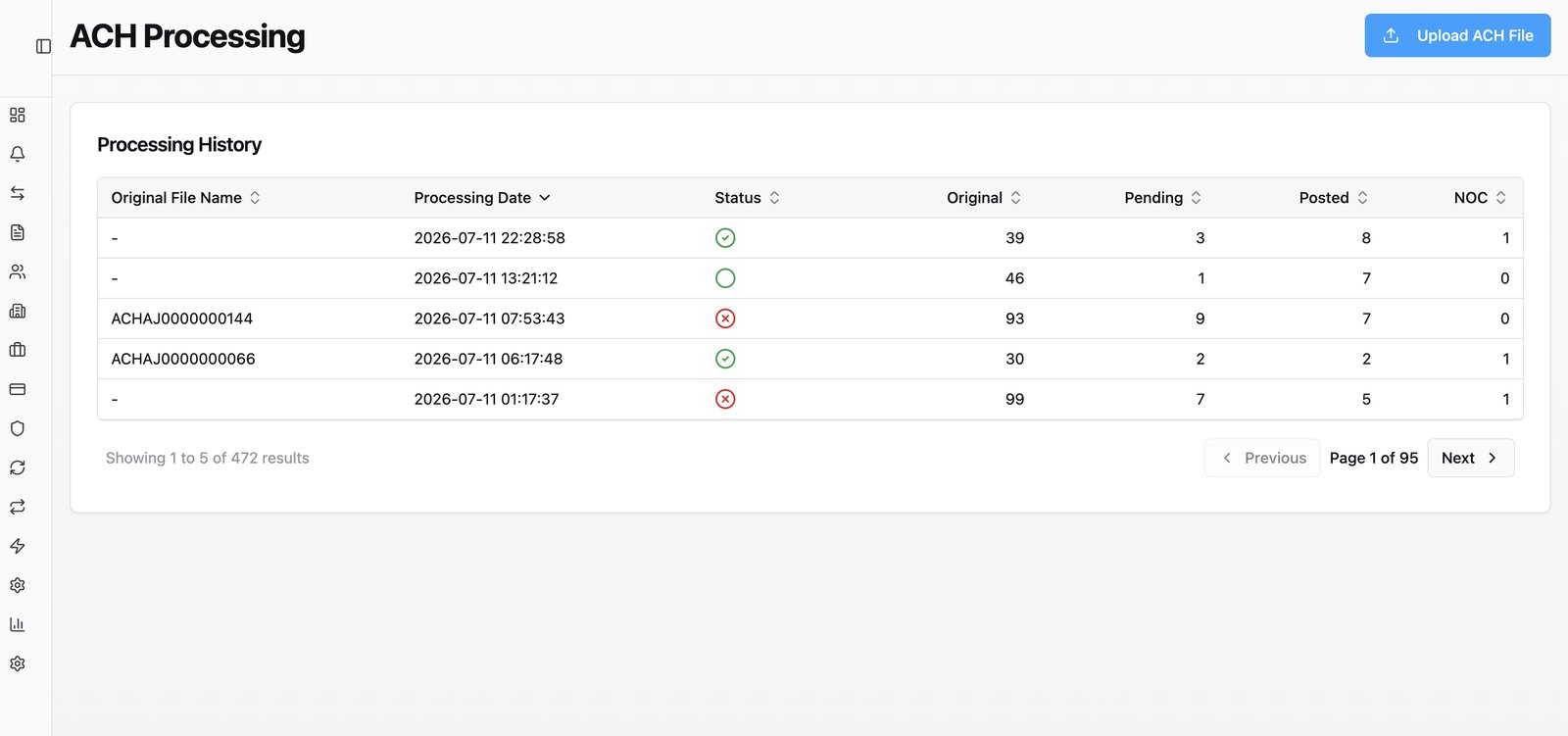

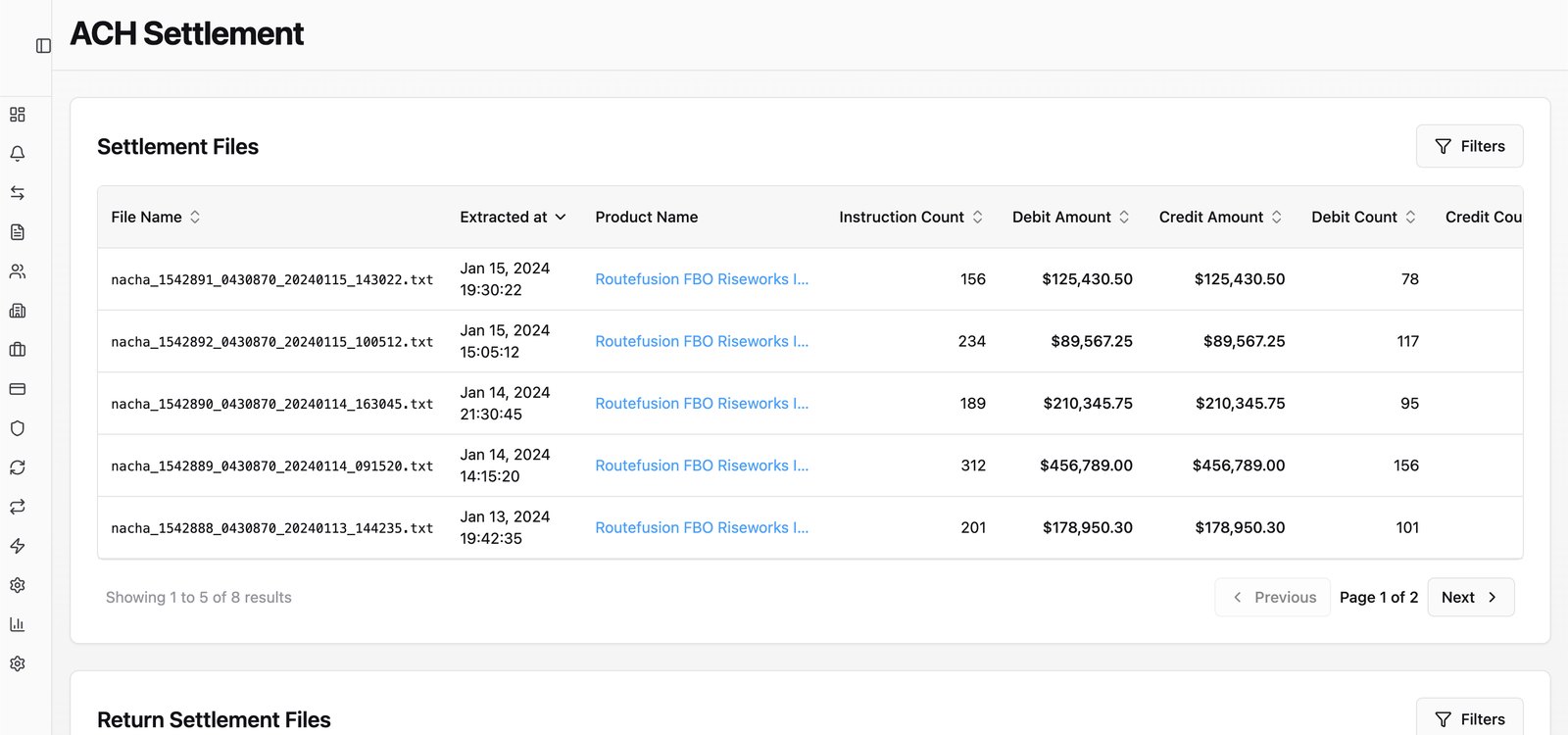

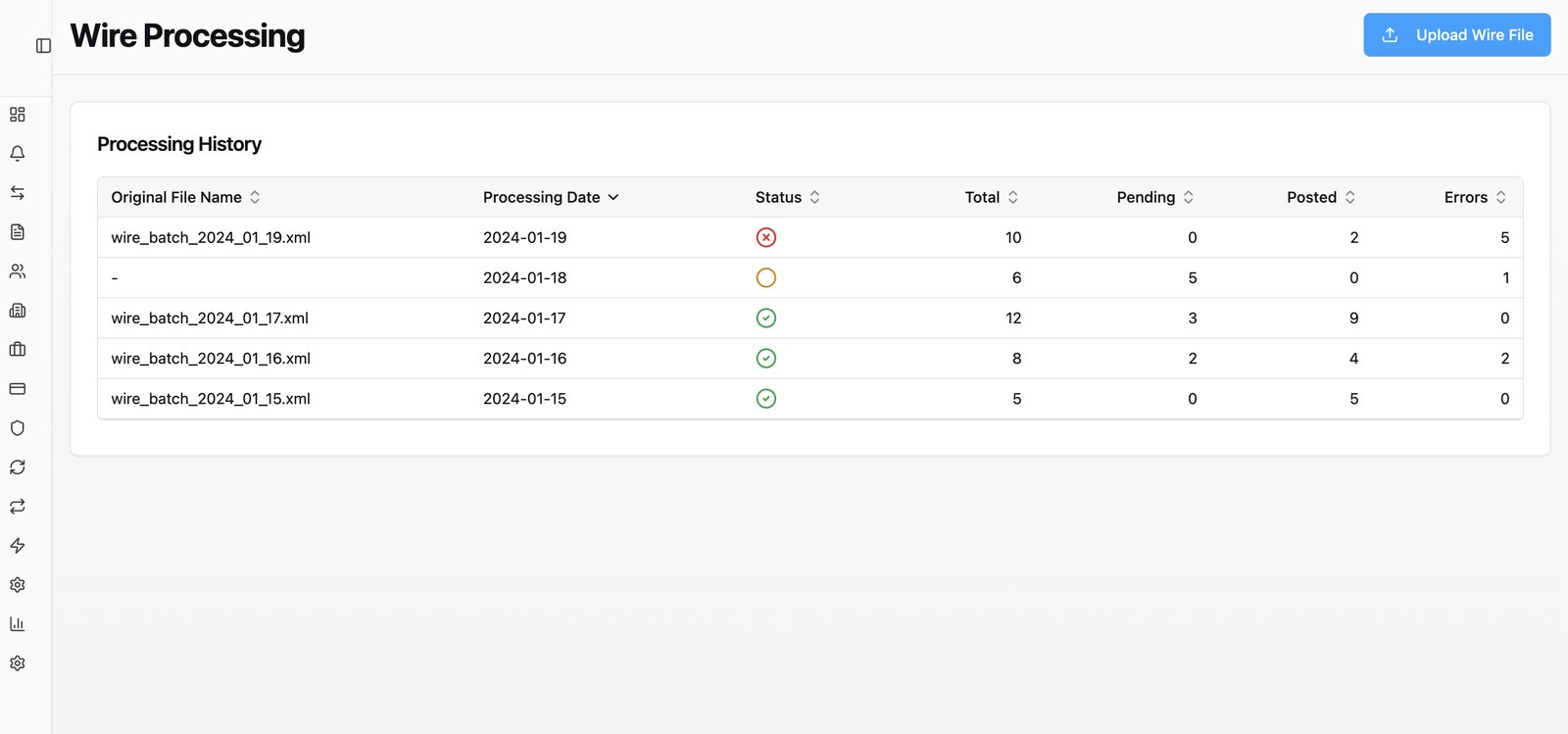

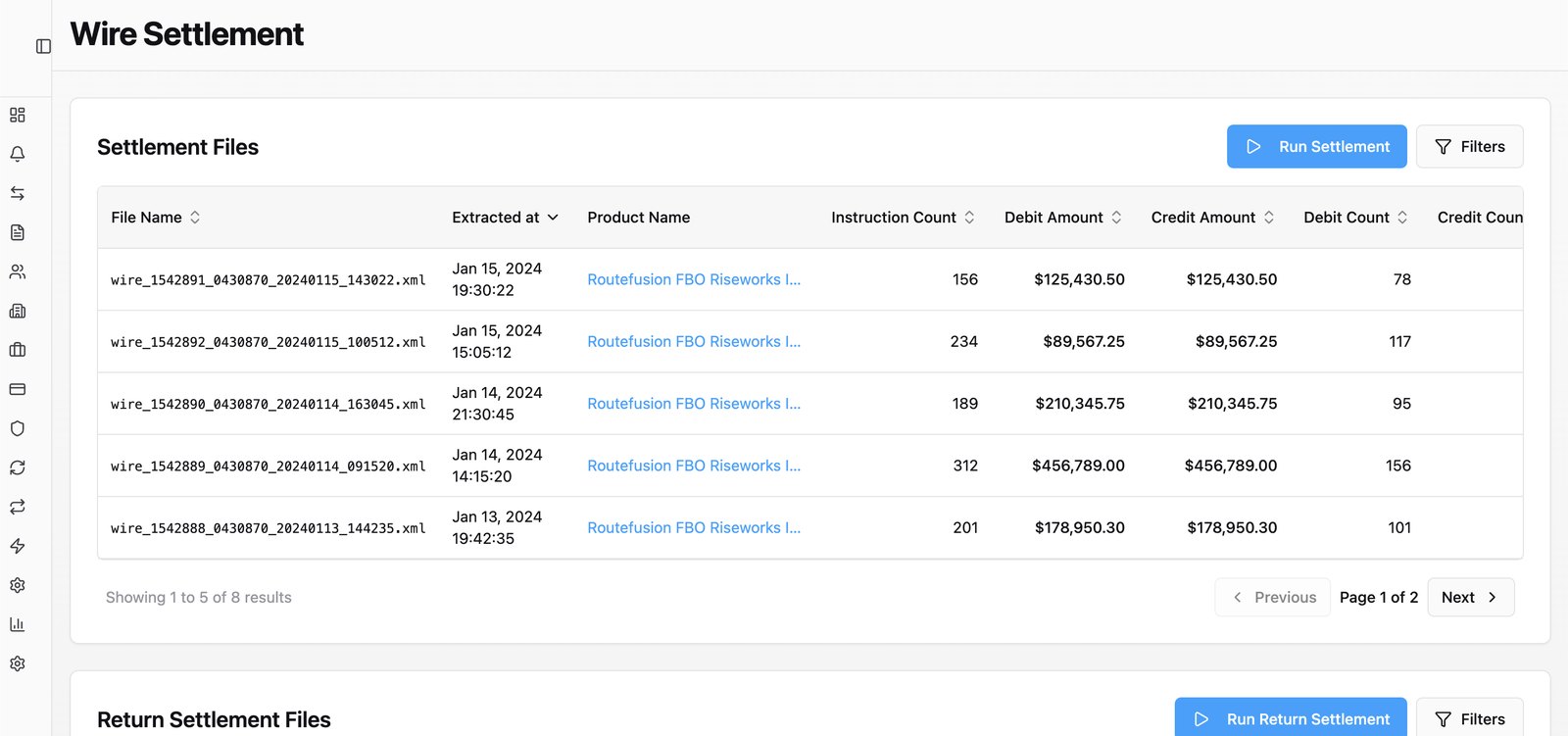

The full lifecycle of money movement. Payments start in a guided create flow — transfer, adjustment, wire, or fee, with counterparty search built in — and every transaction gets a detail view carrying its OFAC check, processing status, and a compliance-reviewed timeline. Behind that sit the rails: ACH and wire file processing with per-file pending, posted, and NOC counts, and settlement runs that reconcile debits and credits down to the file.

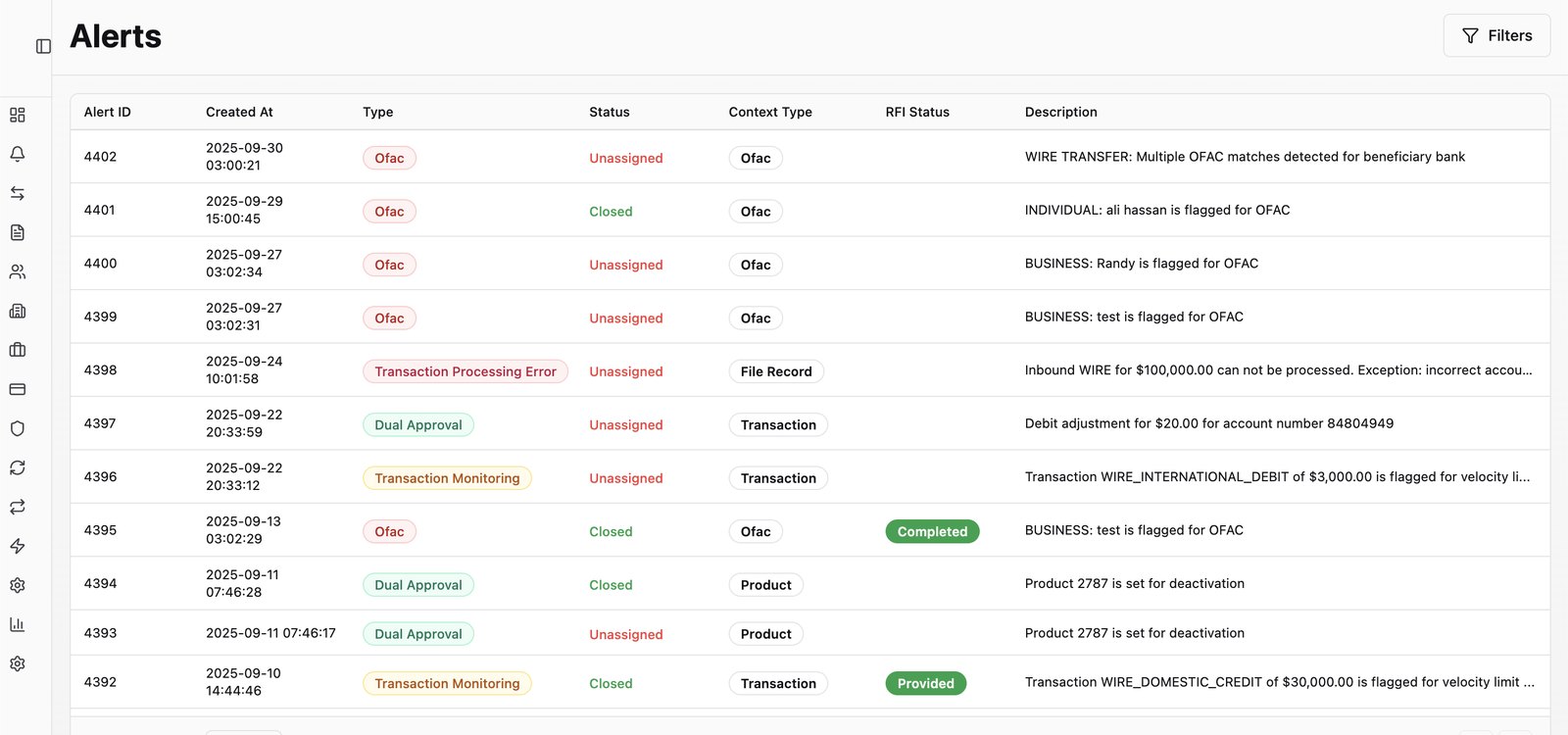

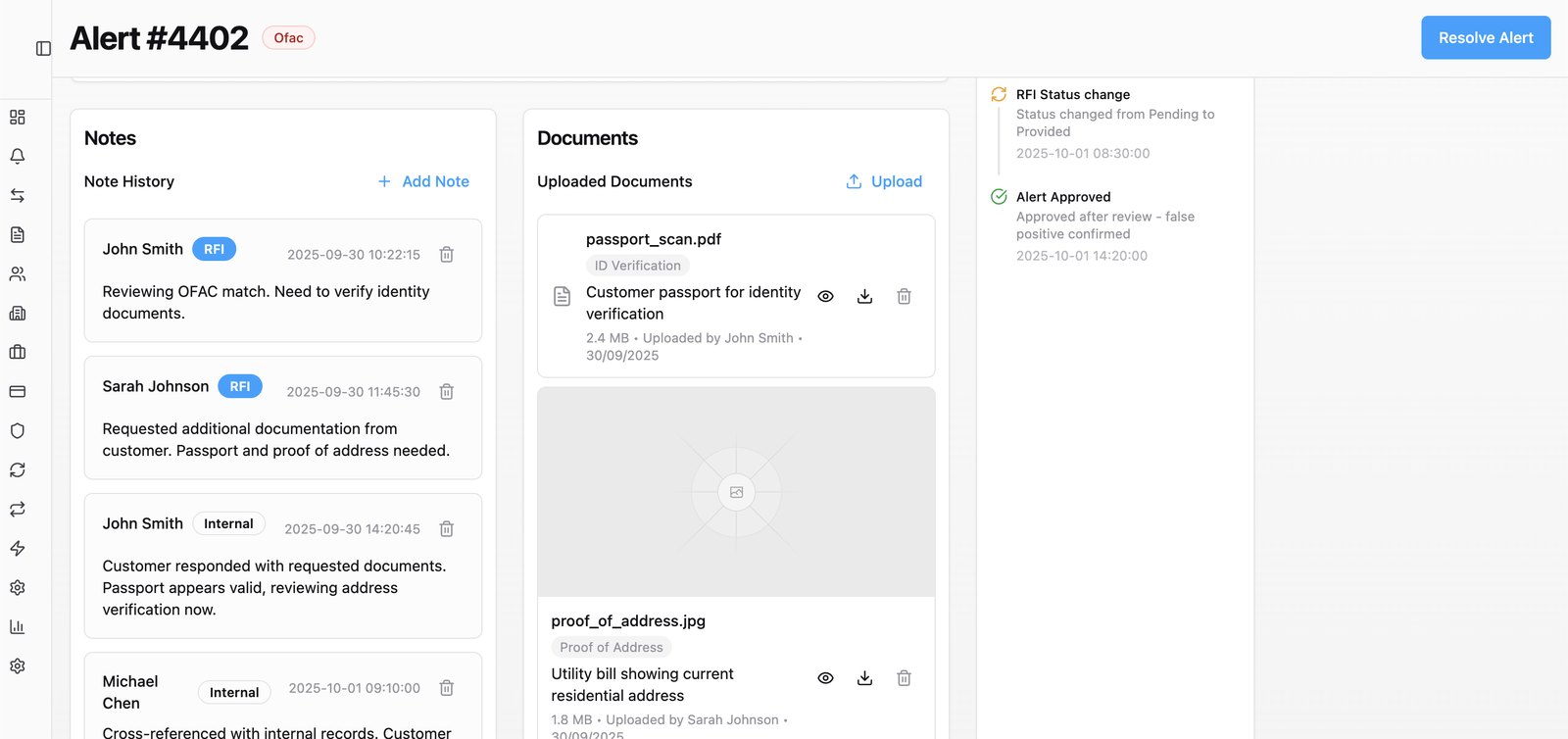

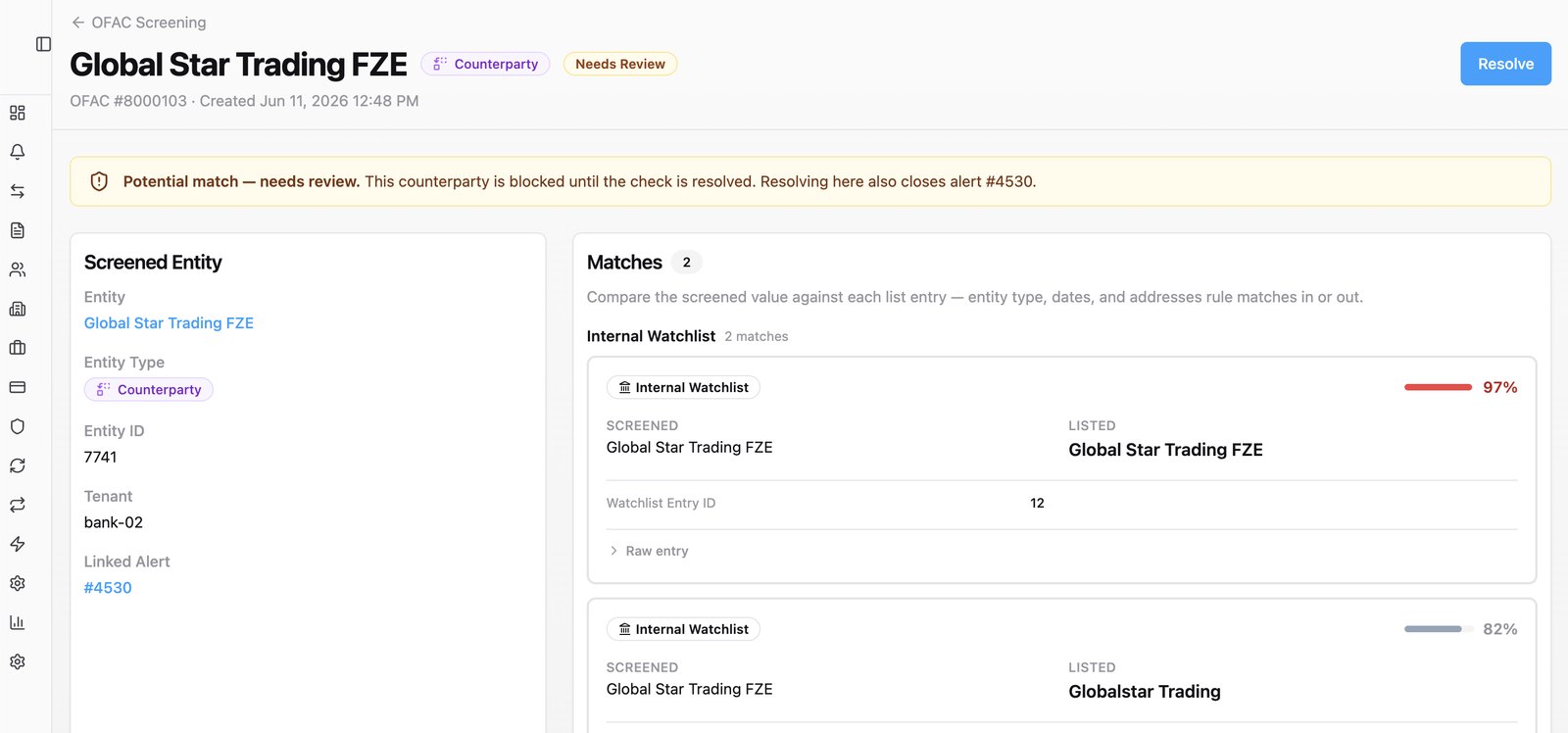

The alerts queue — OFAC matches, dual approvals, and monitoring flags awaiting triage.

Fraud and compliance, one queue

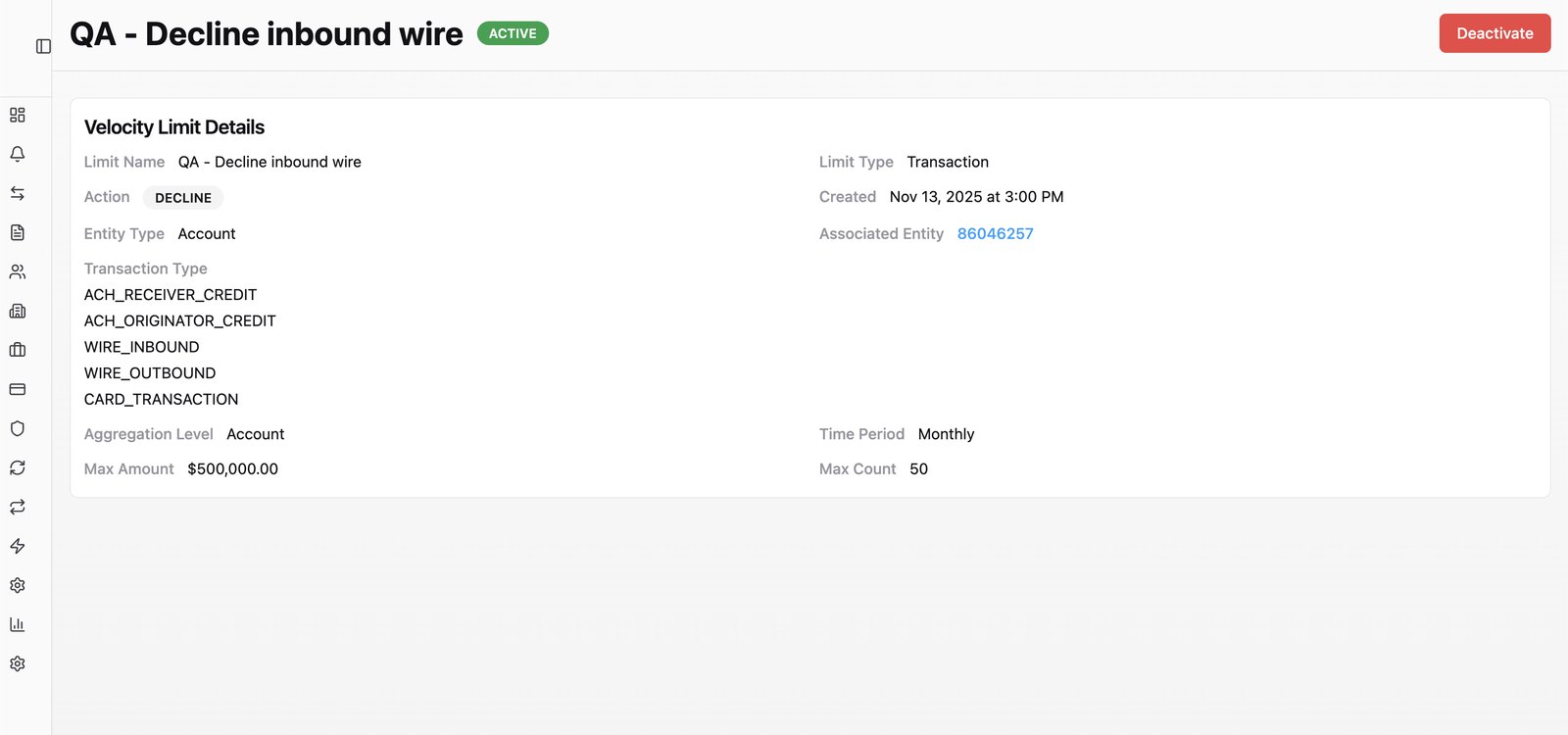

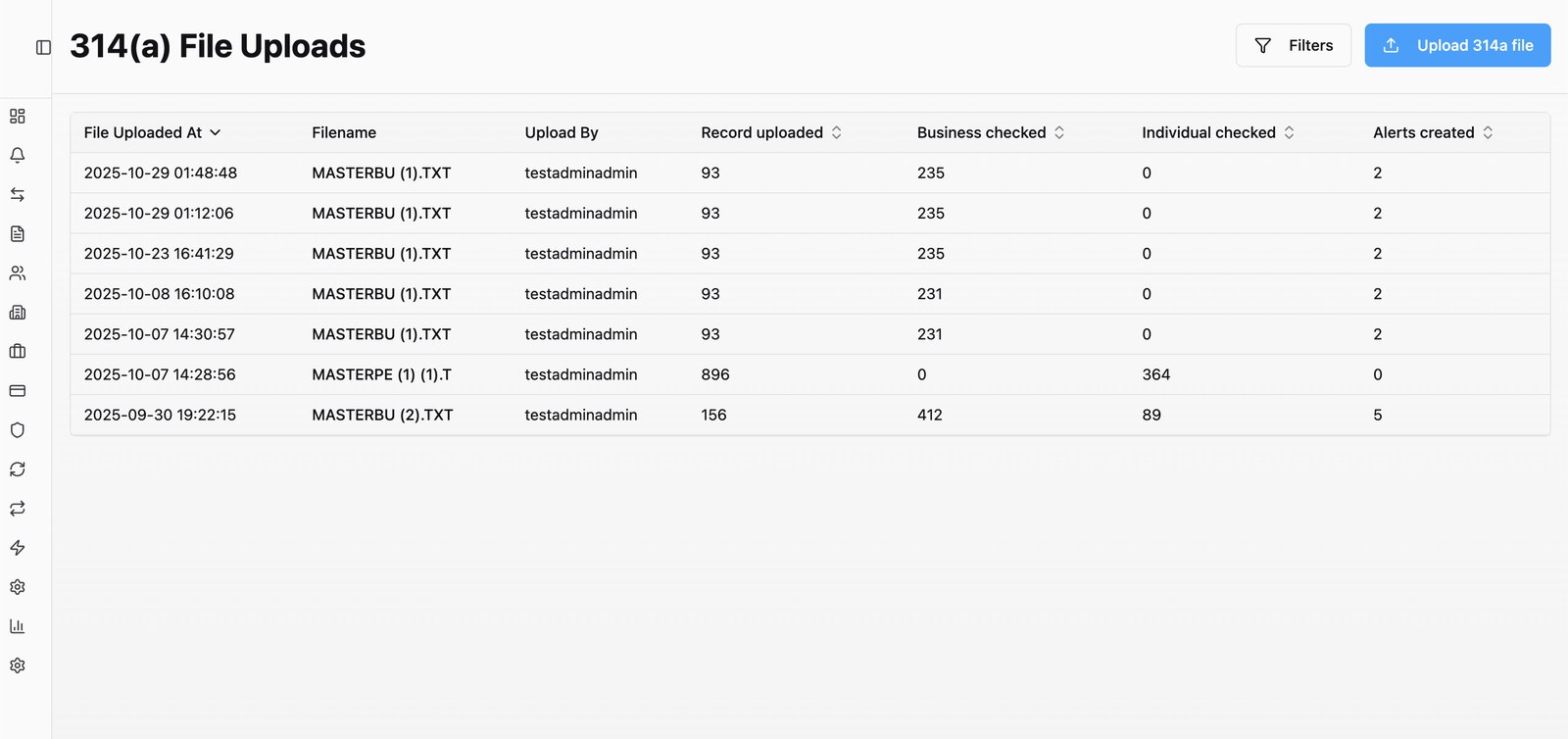

OFAC hits, dual approvals, monitoring flags, and processing errors land in a single alert queue — and each alert opens into a full investigation: analyst notes, RFI tracking, document uploads, and a resolution timeline. OFAC matches come scored against watchlists with the counterparty blocked until reviewed, velocity limits enforce transaction rules automatically, and 314(a) batch screening runs from the same surface.

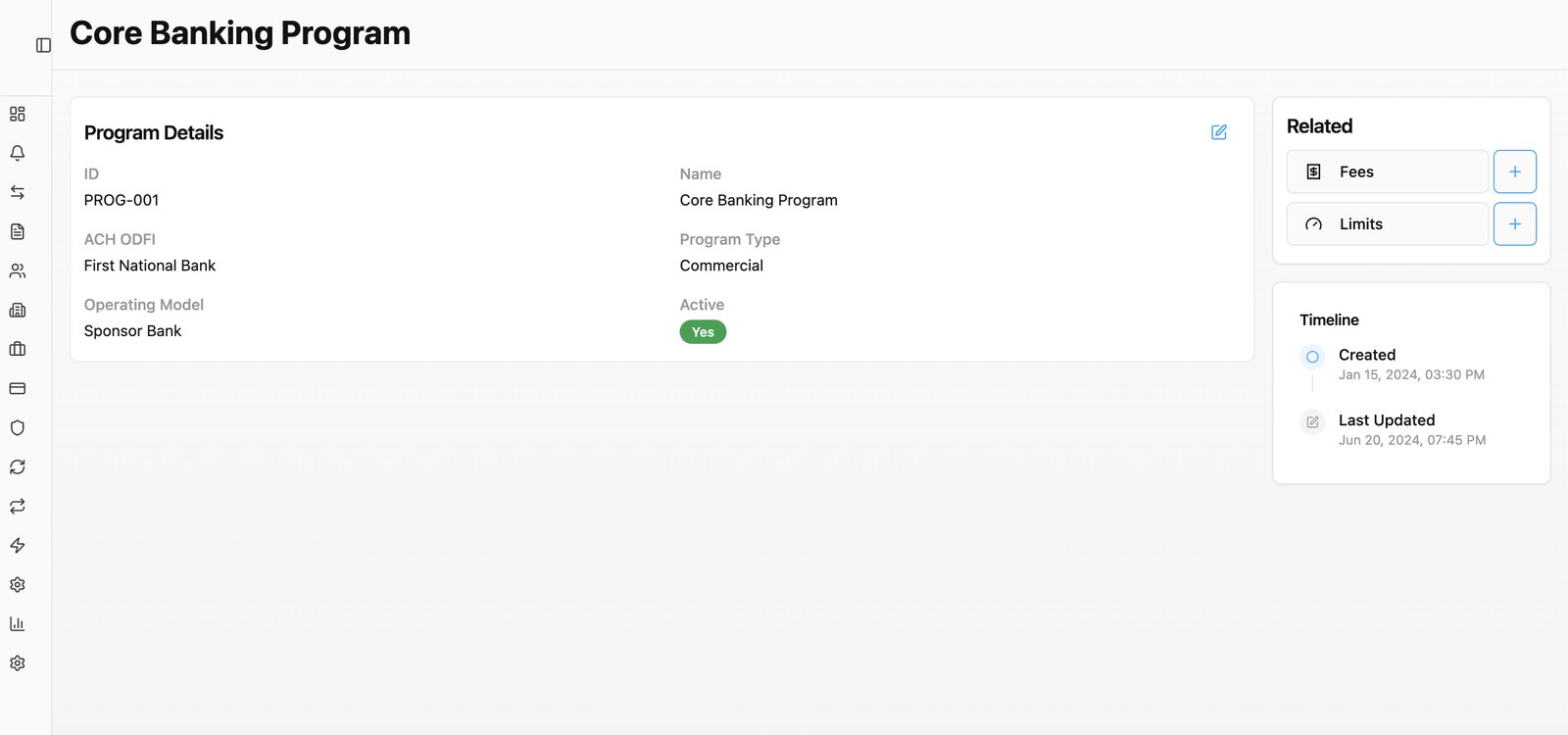

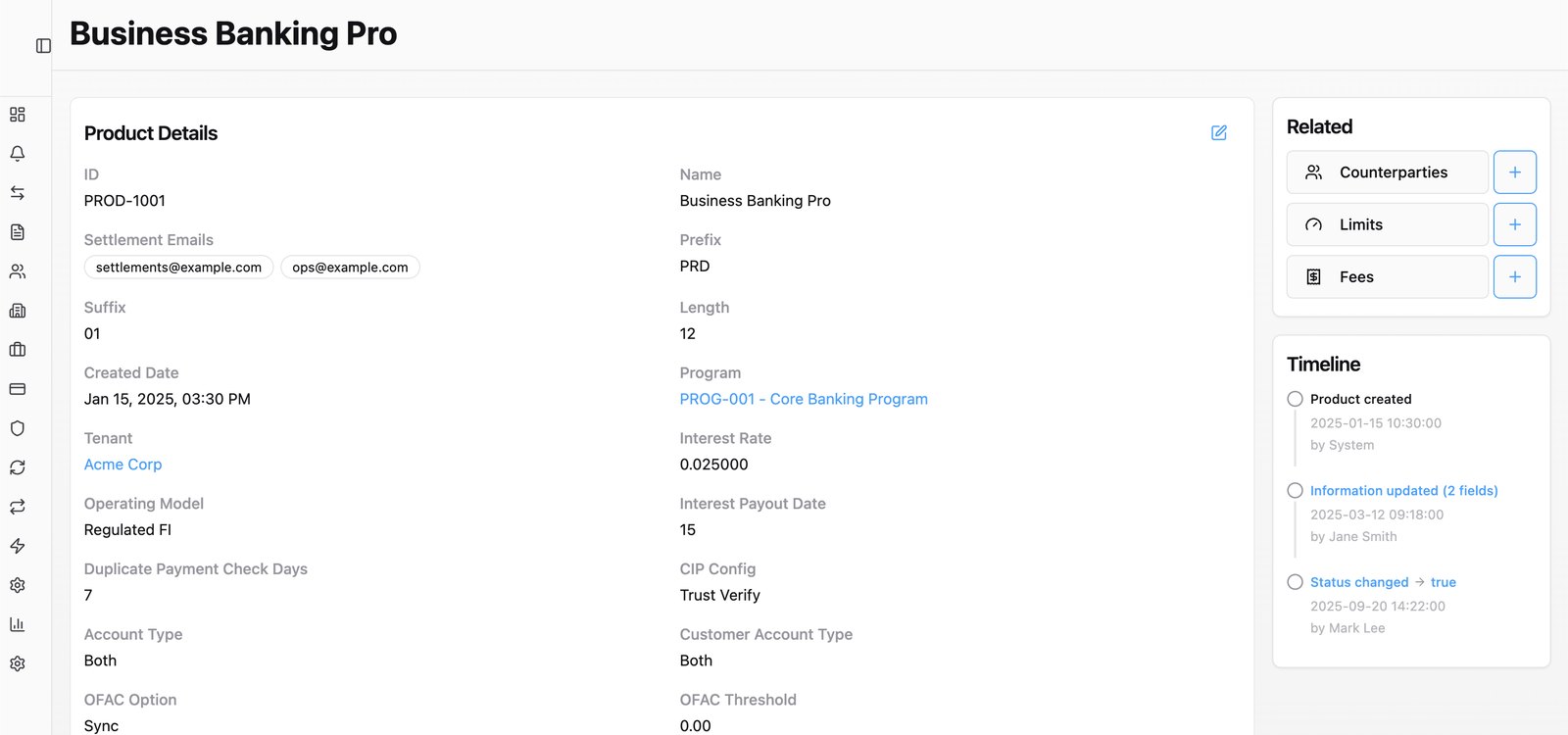

Program configuration — operating model, ODFI, and status.

Programs, products, and the kill switch

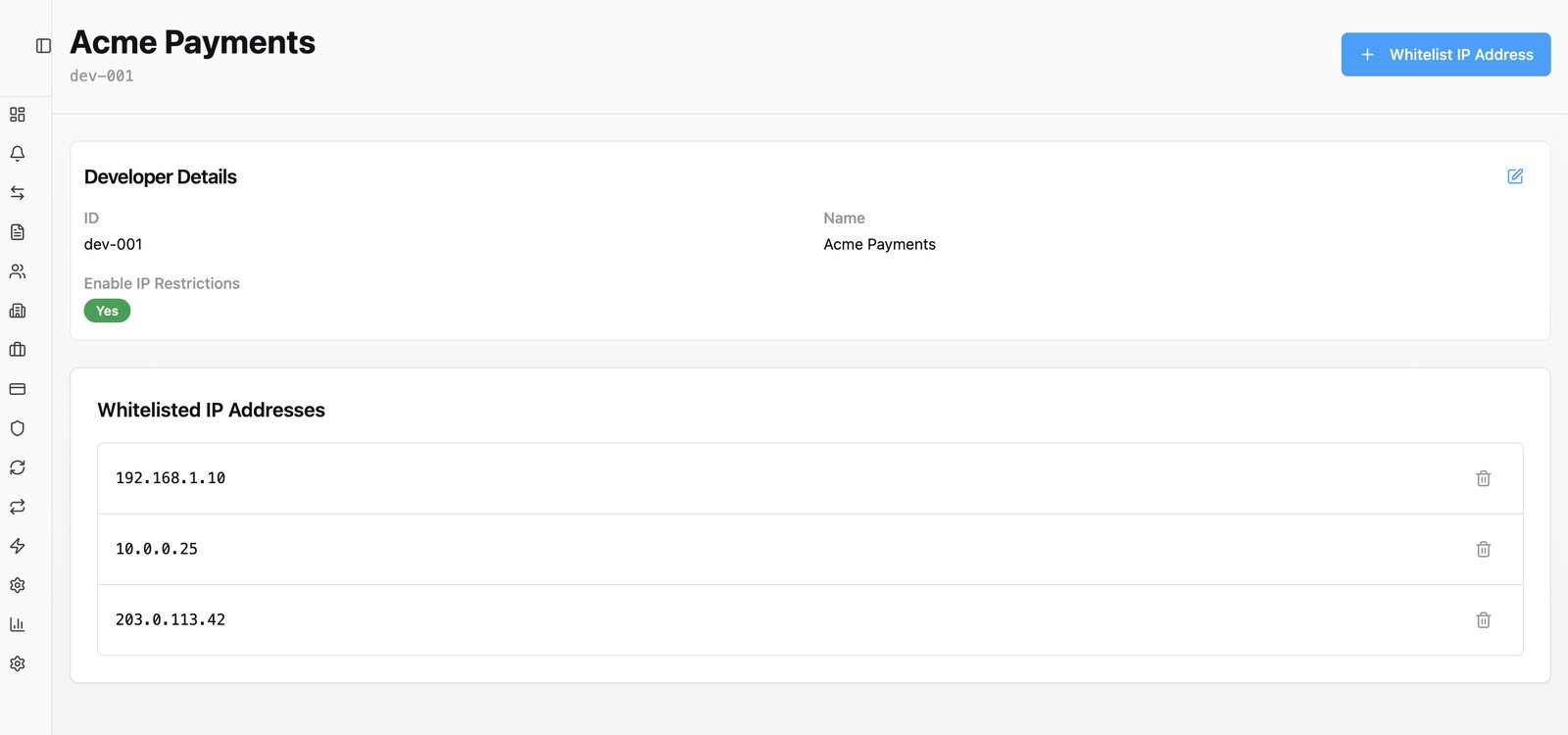

One platform, many programs: banks run multiple fintech programs and product lines side by side — each program with its own operating model and ODFI, each product with its own settlement contacts, CIP configuration, interest terms, and OFAC thresholds, per tenant. Every operational lever stays in the bank's hands, down to API access with IP whitelisting — and the kill switch can pause a program, account, or counterparty instantly.

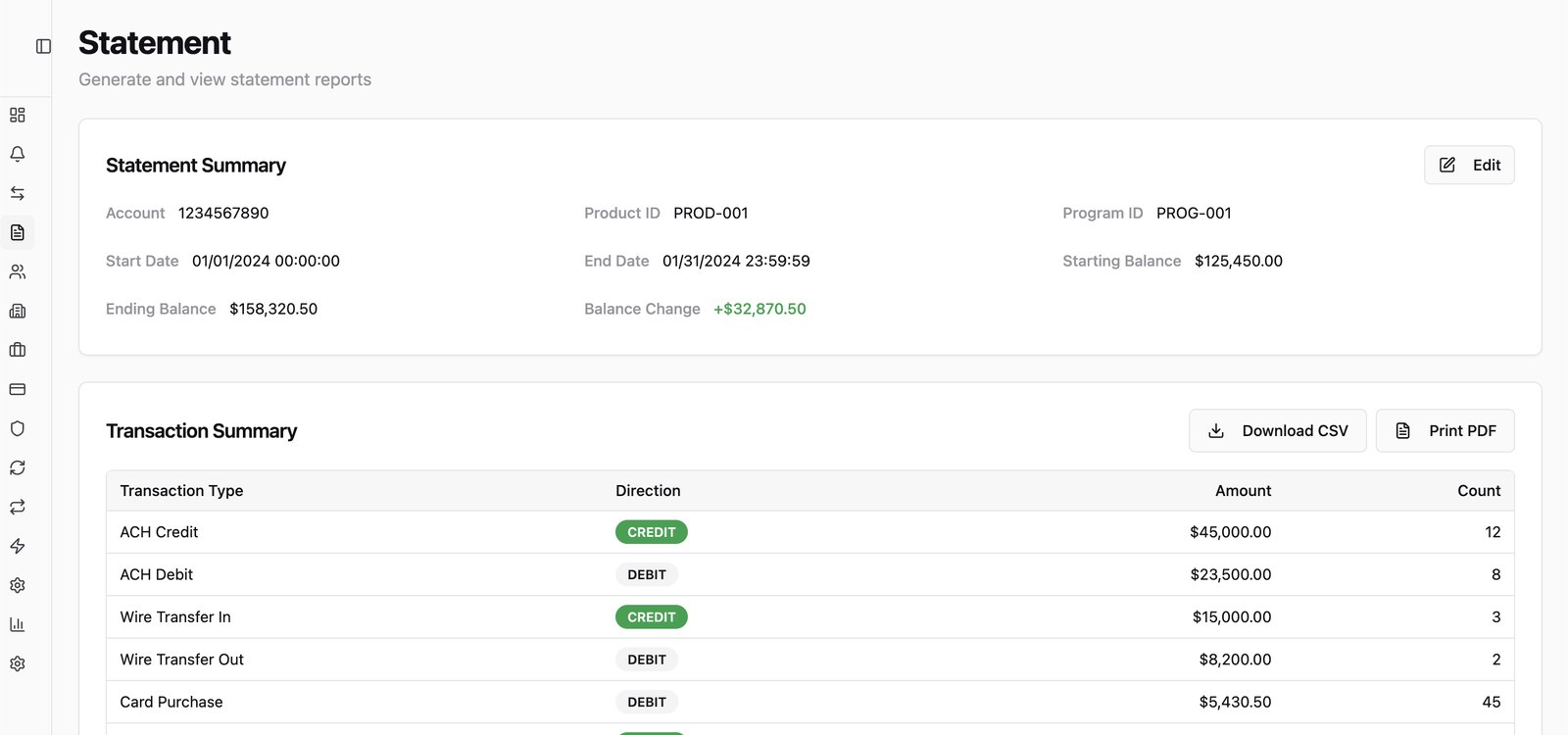

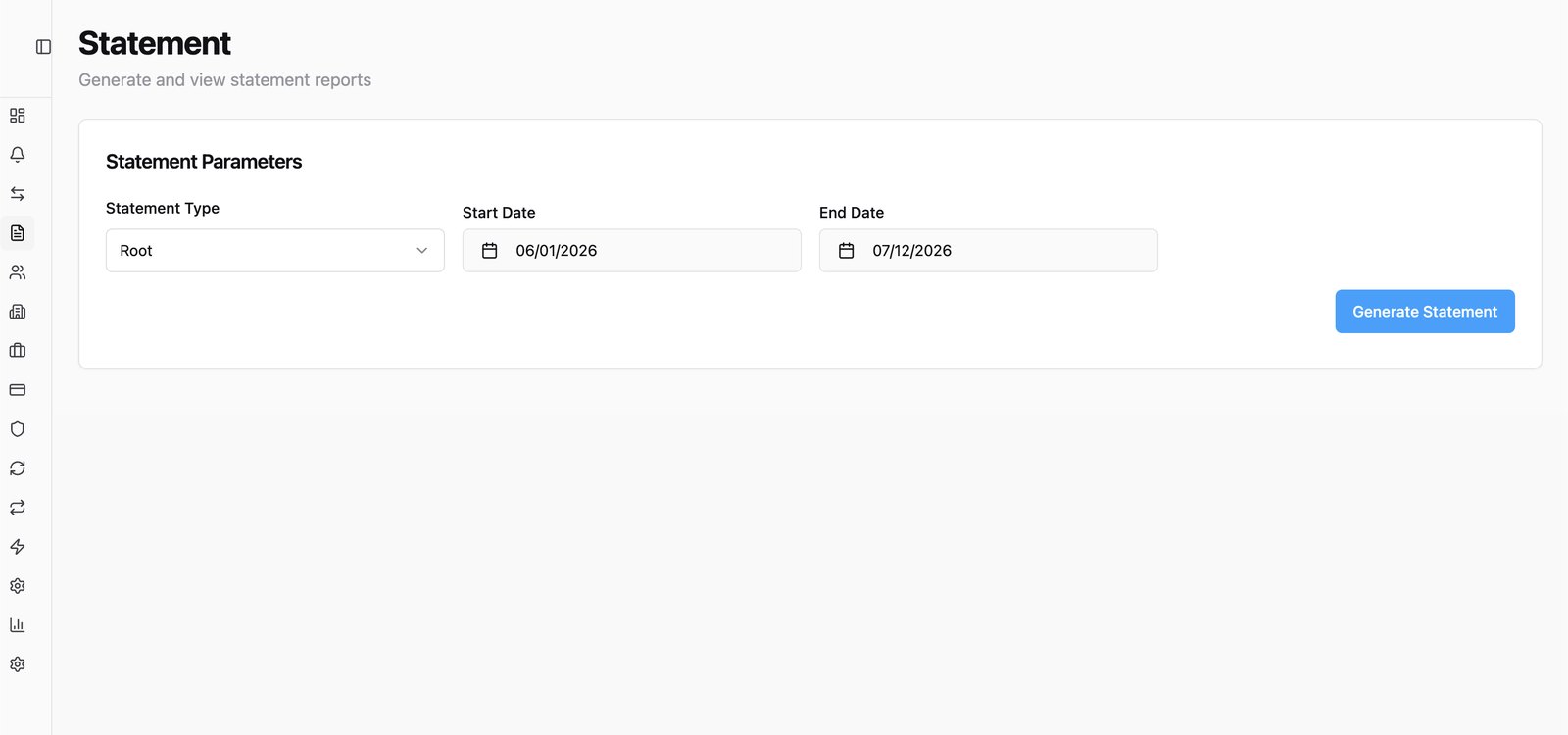

A generated statement — balances, balance change, and per-type transaction summary with CSV/PDF export.

Statements and reporting

Pick an entity and a date range, and the ledger does the rest: a statement summary with starting and ending balances, balance change for the period, and transaction rollups by type and direction — exportable to CSV or PDF. The same ledger data feeds reconciliation uploads and exception review.

Impact

- In production at US and international financial institutions — daily operations, compliance, and risk run through it.

- A single system of record that replaced fragmented legacy tooling.

- Trusted with mission-critical money movement across ACH, wires, FedNow, and RTP.

- Designed, architected, and delivered solo — from UX to backend integrations.